What is US Municipal Infrastructure Debt?

US municipal bonds – a key source of funding for essential public projects

US municipal bonds, also known as muni bonds or munis, are bonds issued by US states, cities or local government bodies. They can take the form of general obligation (GO) bonds, funded via tax revenues, or revenue bonds, secured by an income stream from a specific local infrastructure asset. Historically, this has meant that default rates have been low, and risk adverse investors could consider investing in munis as a way to diversify corporate bond holdings.

The majority of municipal bonds are issued in a format that exempts the holder from US federal income tax, and potentially local state taxes – a significant benefit for many US domiciled citizens and corporates. However, there is a growing section of the municipal bond market that is issued in a fully taxable format – by issuing fully taxable debt, the issuer has greater flexibility on how they can use the proceeds. Taxable municipal bonds generally trade with a higher gross yield than their tax-exempt counterparts, and this has led to an increase in demand from non-US investors.

Today, the US municipal bond market supplies around 80% of the capital needed for US infrastructure maintenance and development[1]. Currently, there are 56,248 issuers in the market; this represents almost USD4 trillion in lending[2].

From an investment perspective, US municipal bonds are seen as a high-quality asset class. Individual US states that issue infrastructure-related bonds might be major economies in their own right, with levels of growth comparable to that of sovereign countries. For example, the gross domestic product of California alone is equivalent to that of the United Kingdom[3].

[1] Source: SIFMA as at 30 June 2021.

[2] Source: SIFMA as at 30 June 2021.

[3] Source: Bureau of Economic Analysis (BEA) and International Monetary Fund as at 31 December 2020.

US Municipal Bonds can offer:

* For BNY Mellon Global Funds, plc, none of the sub-funds which are recognised schemes in Singapore constitute ESG Funds (as defined in the MAS’s Circular No. CFC 02/2022), except for BNY Mellon Sustainable Global Emerging Markets Fund, BNY Mellon Sustainable Global Dynamic Bond Fund and Responsible Horizons EM Debt Impact Fund. Other funds which are not registered for offering to retail investors may or may not constitute ESG funds (where defined in the relevant local jurisdiction).

What does US municipal infrastructure debt typically finance?

Why consider this asset class?

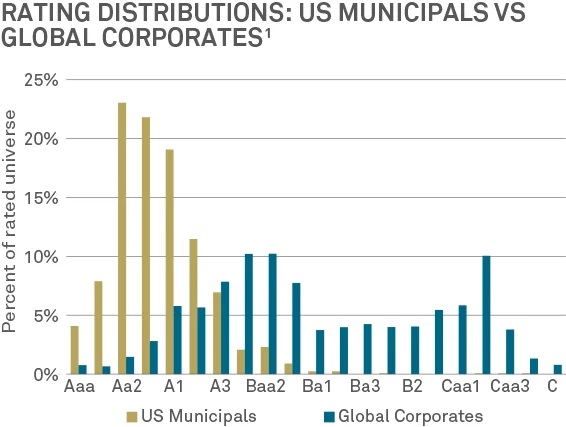

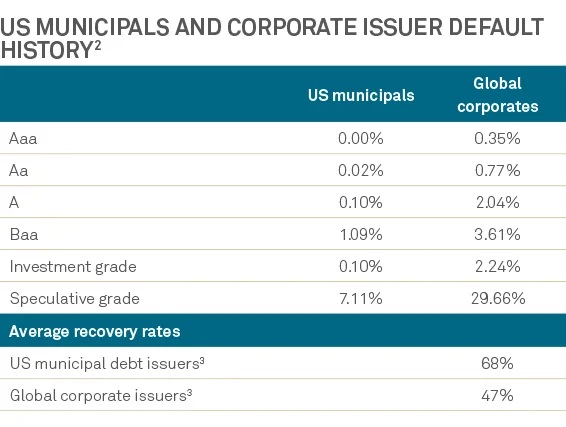

1. Better ratings quality and lower default rates relative to global corporate bonds, with recovery rates that are significantly above average for global corporate issuers.

The left-hand graph below shows the ratings of all US municipal bonds versus global corporate bonds, with ‘Aaa’ being the highest and C the lowest. As you can see, most US municipal bonds fall within the higher-quality end of the ratings scale.

Meanwhile, the right-hand table demonstrates the relatively lower defaults among US municipal bonds in relation to global corporate bonds. It also reveals that recovery rates for municipal bonds are higher than those of senior unsecured global corporate bonds. This means investors may have a better chance of getting some of their money back if a US municipal bond defaults.

Sources: 1. Moody’s Investors Services as at 31 December 2020; 2. Source: Moody’s cumulative default rates by rating category, 1970-2020; 3. Moody’s Investors Service as at 30 September 2020, average corporate debt recovery rates for senior unsecured bonds 1970-202

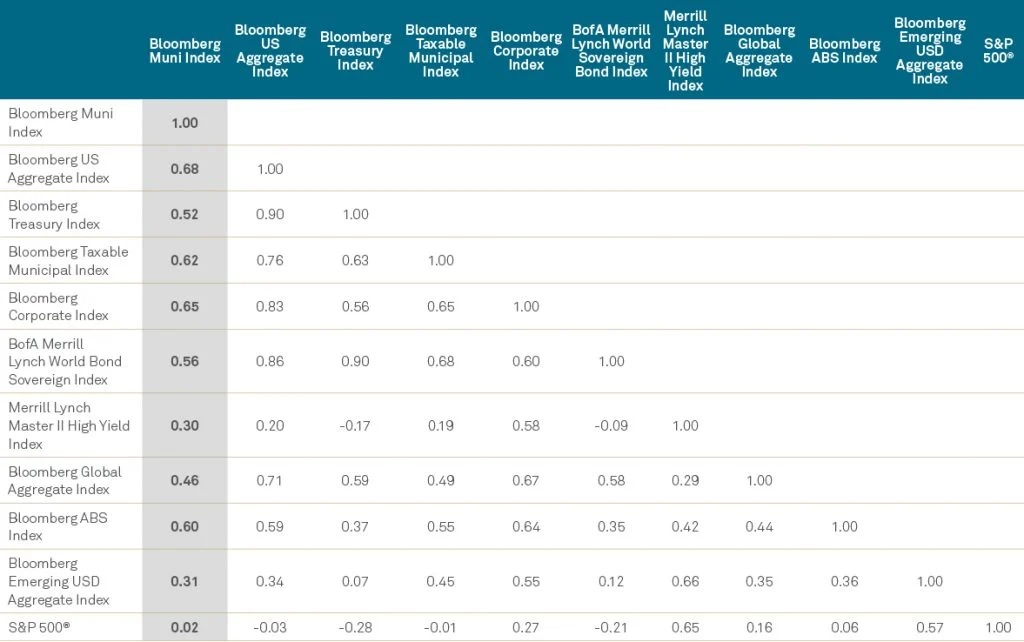

2. Lower correlation to major asset classes

In this table, we show how the performance of the US municipal bond market compares to other types of fixed-income instruments. From January 1997 to September 2021, for every 1% of growth in the US municipal bond market, you would have achieved only 0.68% had the same amount been invested in investment-grade bonds or 0.52% from US Treasuries.

Source: Bloomberg, Barclays, Merrill Lynch as at 30 September 2021. *Correlation matrix based on total returns, since 1 January 1997

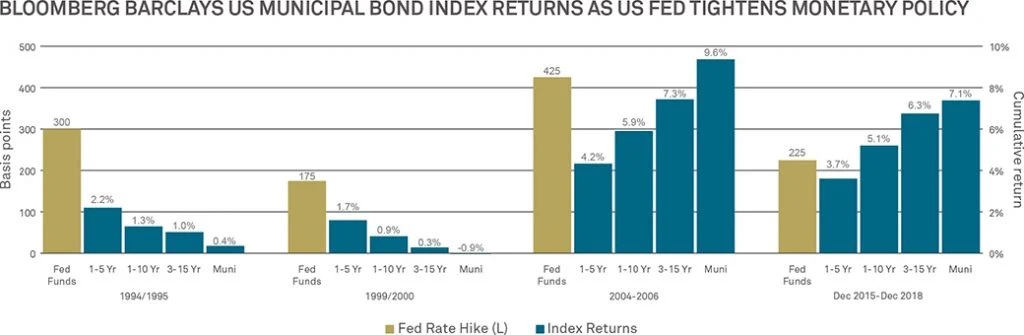

3. Potential to offer protection from US monetary tightening

We often hear the term “monetary tightening”. What this refers to is the process of raising interest rates. Central banks often do this to cool an overheating economy, as higher interest rates make borrowing more expensive. Higher interest rates can also make the interest paid out by some bonds look less appealing, as investors could potentially find higher rates elsewhere.

In the graph below, we show that despite increases in US interest rates, based on historical data, municipal bond performance (including reinvestment of income) were able to deliver positive returns. Investors may consider US municipal bonds in an adverse performance environment for fixed income.

Source: Municipal Market Data MMD, FRED, Bloomberg, firm data as at 30 June 2021. For illustrative purposes only.

Note: the bars labelled “1-5 yr”, “1-10 yr” and “3-15 yr” are representative of the returns of the “1-5 year”, “1-10 year” and “3-15 year” Bloomberg Barclays US Municipal Index respectively. The bars labelled “Muni” are representative of the Bloomberg Barclays US Municipal Index’s total returns in the corresponding years on the X-axis (i.e. 1994/1995, 1999/2000, 2004-2006 and Dec 2015 – Dec 2018). The time periods depicted in the chart are the most recent instances where the Federal Reserve tightened monetary policy, or raised interest rates (as shown by the green bar representing the magnitude of rate hikes). Similarly, the blue bars show the relative performance of several distinct municipal indices during the same time period (delivering positive returns).

Why the BNY Mellon US Municipal Infrastructure Debt Fund?

Launched in 2017, the BNY Mellon US Municipal Infrastructure Debt Fund was one of the first products to invest predominately in taxable and tax-exempt infrastructure-focused US municipal bonds.

Investment objective

The Fund aims to provide as high a level of income as is consistent with the preservation of capital. This is not a capital guaranteed fund and there is no guarantee of the repayment of principal.

Our team’s objectives

By taking a long-term approach to investing, our dedicated US municipal debt team seeks to capture opportunities in the US municipal bond market. The team invests in taxable and tax-exempt municipal infrastructure bonds, enabling it to uncover the holdings which are most likely to help us to achieve the fund’s investment objective.

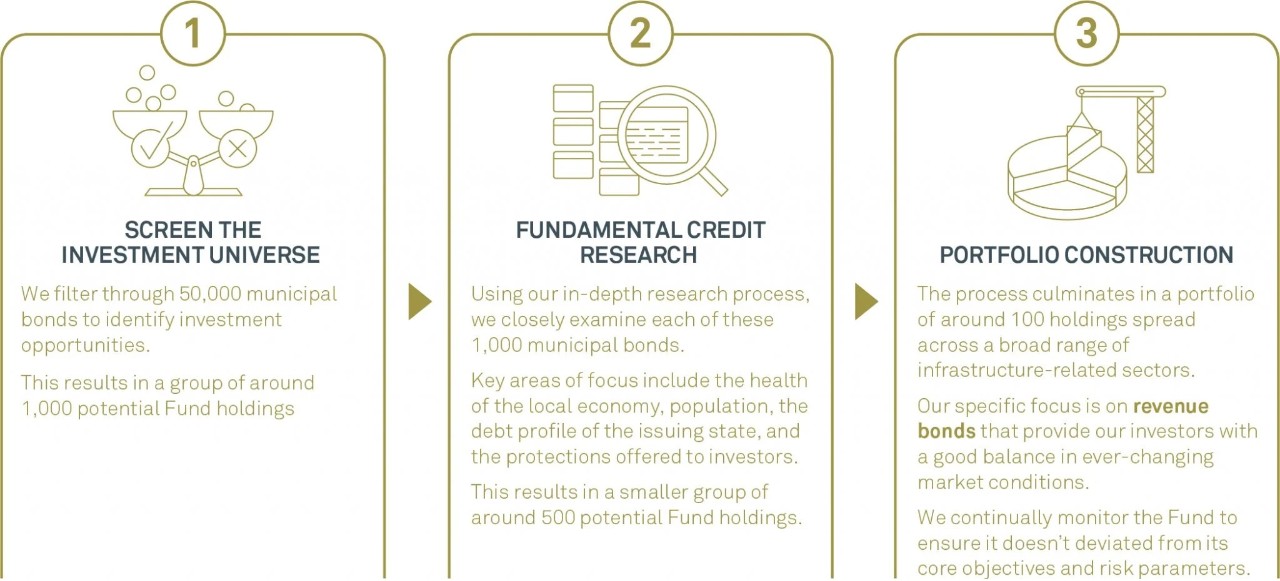

Our investment process

We take a pragmatic, long-term approach to investing. This allows our team to identify bonds that are attractive on a risk-adjusted basis.

Investing for a sustainable future (ESG)

The USD4 trillion municipal bond market is a natural avenue for ESG investing. State and local governments regularly finance numerous long-term public projects that align well with sustainable missions led by prudent and responsible governance.

Our team of senior sector and region-specific research analysts formulate recommendations based on myriad

fundamental credit factors including traditional metrics such as balance sheet, economic/tax base, financial metrics and bond covenants. Beyond traditional metrics, our analysts consider key ESG risk and opportunity themes across a wide subset of sectors. Our proprietary Muni ESG analytical framework breaks down ESG risks into five key themes: climate change, aging US infrastructure, natural resource scarcity, demographic shifts and governance.

These risks have credit and fiscal implications for a municipality’s spending, debt, revenues, liquidity, and rainy-day

reserve profiles. Careful consideration of these factors, along with traditional fundamental credit metrics, trading

levels and ratings analysis, are key to our bond selection process.

About the Fund

Available share classes

| Share class | Minimum initial investment | ISIN | Bloomberg code | Factsheet | Benchmark | Launch date |

| Euro H (Acc.) (hedged) | EUR5,000 | IE00BDCJYF87 | BNUMEHA | 50% Bloomberg Barclays US Municipal Bond Total Return Index, 50% Bloomberg Barclays Taxable US Municipal Bond Total Return Index | 29 May 2020 | |

| Euro H (Inc.) (hedged) | EUR5,000 | IE00BDCJYG94 | BNUMEHI | 29 May 2020 | ||

| USD W (Acc.) | USD15,000,000 | IE00BDCJZ442 | BNUMUWA | 19 February 2019 | ||

| USD W (Inc.) | USD15,000,000 | IE00BDCJZ558 | BNUMUWI | 29 May 2020 | ||

| USD A (Inc.) | USD5,000 | IE00BDCJY817 | BNMIDAI | 29 October 2021 | ||

| USD A (Acc.) | USD5,000 | IE00BDCJY700 | BMUIDAU | 29 May 2020 | ||

| USD A (Inc.) (M) | USD5,000 | IE00BMQBXD40 | BMUSMAI | 28 January 2021 | ||

| SGD W (Inc.) (M) | SGD15,000,000 | IE000KVZ81R6 | BNUMUSW | 14 October 2022 |

Investment risks

- General obligation bonds risk — general obligation bonds are secured by the full faith, credit, and taxing power of the municipality issuing the obligation. As such, timely payments depend on the municipality’s credit quality, ability to raise tax revenues and ability to maintain an adequate tax base.

- Revenue bonds risk — revenue bonds with payments depend on the money earned by the particular facility or class of facilities, or the amount of revenues derived from another source. If the specified revenues do not materialize, then the bonds may not be repaid.

- Adverse economic, political or regulatory changes or adverse factors such as additional costs, competition, environmental concerns, taxes, and changes in end-user numbers in infrastructure sectors and projects can significantly affect the revenue generated and the overall market. This may lead to defaults on payment of principal or interest of the municipal bonds. The federal government of the US are not obliged to support any municipal bonds in default. The Fund could suffer substantial loss.

- There are specific risks associated with municipal bonds including different disclosure requirements, lesser degree of transparency compared to other bond markets. Municipal bonds may also be subject to call or prepayment risks. There are specific risks associated with certain municipal sectors that the fund may invest, including general obligation bonds risk, revenue bonds risk, private activity bonds risk, moral obligation bonds risk, municipal notes risk and municipal lease obligations risk.

- The Fund invests primarily in municipal bonds, which are issued by a state, municipality, not-for-profit corporate issuers of the United States of America (the US) to finance infrastructure sectors and projects conducted in the US.

- The Fund Investment portfolio may fall in value and there is no guarantee of the repayment of principal.

- Adverse economic, political or regulatory changes or adverse factors such as additional costs, competition, environmental concerns, taxes, and changes in end-user numbers in infrastructure sectors and projects can significantly affect the revenue generated and the overall market. This may lead to defaults on payment of principal or interest of the municipal bonds. The federal government of the US are not obliged to support any municipal bonds in default. The Fund could suffer substantial loss.

- There are specific risks associated with municipal bonds including different disclosure requirements, lesser degree of transparency compared to other bond markets. Municipal bonds may also be subject to call or prepayment risks. There are specific risks associated with certain municipal sectors that the fund may invest, including general obligation bonds risk, revenue bonds risk, private activity bonds risk, moral obligation bonds risk, municipal notes risk and municipal lease obligations risk.

- The Fund is exposed to risks associated with debt securities, including credit risk, interest rate and inflation risk, downgrading risk, credit rating risk and sub-investment grade debt securities risk.

- The Fund’s investments are concentrated in the US and may be more susceptible to adverse economic, political, policy, foreign exchange, liquidity, tax, legal or regulatory events affecting the United States.

- The Fund may pay dividends effectively out of capital which amounts to a return or withdrawal of part of an investor’s original investment or from any capital gains attributable to that original investment. Any such distributions may result in an immediate reduction of Net Asset Value per share.

- The Fund may invest in derivatives that are volatile, involve special risks such as risk of disproportionate loss due to leverage, counterparty/credit risk, liquidity risk and valuation risks.

- Investors should not rely solely on this document to make investment decisions. Please read the offering documents carefully for further details, including risk factors.

Past performance is not indicative of future performance. The value of investments and the income from them is not guaranteed and can fall as well as rise due to stock market and currency movements. When you sell your investment you may get back less than you originally invested.

This Fund is a sub-fund under BNY Mellon Global Funds, plc (the “Responsible Person”), which is an openended umbrella investment company with variable capital incorporated in Ireland with segregated liability between sub-funds and authorised by the Central Bank of Ireland. The Fund is recognised for retail distribution in Singapore under Section 287 of the Securities and Futures Act 2001. The Responsible Person has appointed BNY Mellon Investment Management Singapore Pte. Limited (“BNYM-IM-SG”) as its Singapore Representative. The prospectus in relation to the Fund is available and a copy of it may be obtained from http://www.bnymellonimapac.com/sg/funds or at BNYM-IM-SG’s distributors. A potential investor should read the prospectus before deciding whether to subscribe or purchase units in the Fund. The value of the units in the Fund and the income accruing to the units, if any, may fall or rise. The net asset value of the Fund is likely to have a high volatility due to its investment policies or portfolio management techniques.

This document shall be used in Singapore only and shall not be used for the purpose of an offer or solicitation in any other jurisdiction or in any circumstances in which such offer or solicitation is unlawful or not authorised. All information herein is made for information purposes only and subject to change at any time without notice, and should not be construed as investment advice or recommendation.

Investors should seek relevant professional/financial advice before investing in the Fund and should read this document in conjunction with the prospectus of the Fund. The Responsible Person, BNYM–IM-SG and its affiliates are not responsible for any advice given to investors. Investments involve risks. A complete description of risk factors is set out in the Prospectus.

Past performance is not a guide to future performance. The value of investments and the income from them is not guaranteed. The Fund may invest in financial derivatives. When you sell your investment you may get back less than you originally invested. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

Issued by BNYM-IM-SG (Co. Reg. No. 201230427E)

AP4151-19-01-2024 (12M)