Source: Bloomberg, Factset as of 31 December 2023

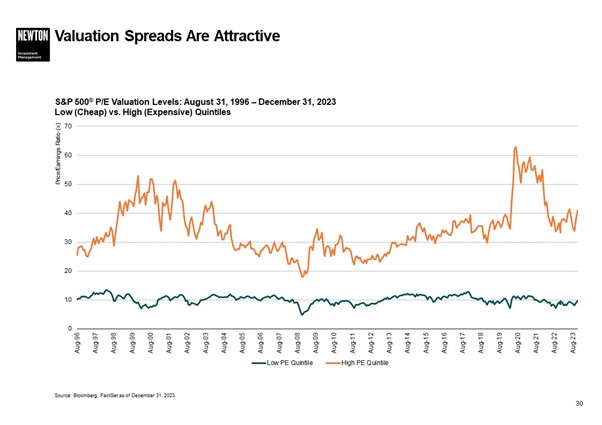

Bailer flags the wide gap between the most expensive and the cheapest quintiles of stocks in the S&P 500 (based on P/E valuation levels). The cheapest quintile looks cheap historically relative to the most expensive quintile, he says. But this group also appears cheap relative to its own history, he adds, with a P/E of about 9.5x compared with an historic average of about 10x4 (see chart above).

Against this backdrop, Bailer says the Newton US equity income team is seeing opportunity in quality companies that trade at high free cashflow yields and low P/E multiples that look attractive from an intrinsic valuation perspective.

“There are opportunities to get value characteristics in the US market right now,” he adds. “We really think there is a huge opportunity to diversify your portfolio into those low P/E stocks and stay away from some of those expensive names that are populating the S&P 500 index.”

Sectors

Bailer highlights financials and energy as two sectors where the team is seeing value opportunities.

He says energy companies have good balance sheets and generate significant amount of free cashflow with little, or no, net debt. Oil supply and demand is well balanced leading to sustainability attractive oil prices, he adds.

Energy stocks are also attractive from a dividend perspective, says Bailer. “We're finding a lot of opportunities in the energy space are delivering a lot of cash back to shareholders in the form of dividends,” he adds.

He notes energy accounts for just 4.6% of the S&P 500 market cap but 11.1% of the S&P 500 index’s income5. Similarly, Bailer says the financials sector accounts for 21.6% of the S&P 500’s income but only 13.2% of the index’s market capitalisation6. He says within financials the team sees opportunities in insurance companies and certain banks.

“We think the stocks are inexpensive, have good risk/reward and pay high dividend yields that are sustainable and can grow,” he adds.

By contrast, Bailer observes the Magnificent Seven stocks on their own account for 28.3% of the S&P 500 index by market cap but generate just 16.9% of the income7.

Dividend growth

Bailer says the US market has relatively low payout ratios versus history, but he thinks these ratios have room to move higher. “You might not have as high dividend yield in the US but importantly you have good dividend growth prospects which can offset some of the inflationary pressures,” he adds.

“That is what we think is different about equity income compared with fixed income. Equity income does not have fixed coupons and can grow over time, and we think the US is one of the best places to show that dividend growth over the next five, 10 years because of the low payout ratios,” he concludes.