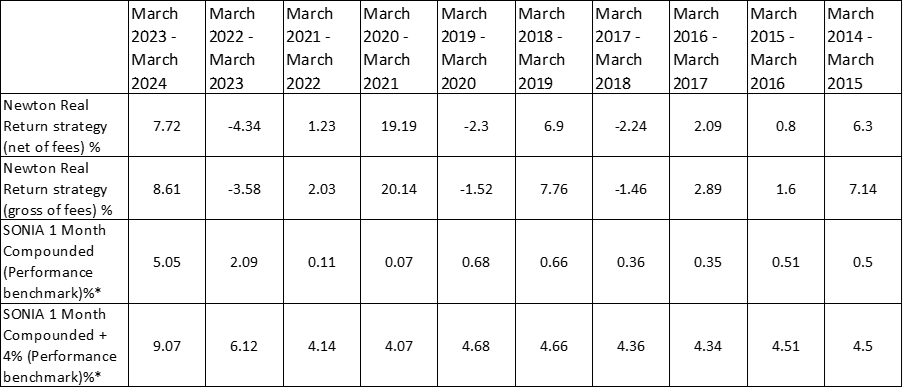

The genesis of the Real Return strategy, when it was first set up in 2004 under the leadership of former Newton veteran Iain Stewart, centred on the concept of a long-term savings vehicle that should be highly flexible and exhibit asymmetry of return by balancing participation in risk-asset markets with a strong emphasis on capital preservation. Rather than relying on models to forecast market returns, insight and perspective were gained through long-term thematic research, allowing the team to make sense of a complex, interconnected world and provide ideas for security selection. Risk was defined as a permanent loss of capital rather than volatility which, although commonly used as a risk proxy, may in fact represent an opportunity.

The global financial crisis and its aftermath

Much of the first ten years of the strategy’s existence was dominated by the fallout from the 2007-8 global financial crisis, an extended cycle prolonged by repeated waves of monetary largesse and supressed volatility, and characterised by historically low interest rates.

During the run-up to the crisis, the team foresaw challenges within many major economies, namely the build-up of debt and excess leverage in the financial system, and indeed this development was encapsulated in the Newton ‘debt and credit’ theme.

The acid test for the strategy occurred in 2008 when the financial crisis unfolded in full force. The strategy was able to benefit from a combination of its direct equity protection, significant cash exposure diversified out of sterling into safe-haven currencies, and indirect hedges in the form of call options on government bonds and gold. It was during this period that the appeal of having a fully flexible strategy was appreciated by clients, while the shortcomings of pursuing an equity index-tracking strategy were keenly felt. The strategy ended 2008 in positive territory, amid carnage in equity markets.

The team quickly capitalised on attractively valued securities during the indiscriminate sell-off that ensued, and the period served as something of a blueprint for how to make full use of the wide range of tools available. Indeed, the success of the strategy gave rise to US-dollar and euro versions, launched in 2009 and 2010 respectively, in response to demand from international investors.

The strategy further evolved in 2018 with the creation of a separate sustainable version, in recognition of the priorities of a subset of clients. This version of the strategy focuses not only on seeking to deliver a long-term performance objective, but also on investing in issuers that positively manage the material impacts of their operations and products on the environment and society.