High yield bonds can potentially form an important component of a portfolio, providing diversification and enhanced yields compared to core government and investment grade corporate bonds.

High yield bonds can form an important component of a portfolio, providing diversification and enhanced yields compared to core government and investment grade corporate bonds.

Current market characteristics are attractive (higher interest cover, lower leverage, fewer maturities in the next few years), leading to the potential for higher risk-adjusted yields; and they provide access to industries and issuers not available in the investment grade universe, enhancing diversification.

High yield opportunity

High yield bonds, also known as sub-investment grade bonds, are a form of corporate debt with a credit rating of below BBB-

Typical reasons why investors may have historically avoided the asset class include higher default risks and increased volatility, poor liquidity/higher trading costs, and lack of specialist expertise.

We highlight three strategies to access the asset class and how some of the above issues can be mitigated for investors, allowing them to incorporate these types of bonds into their portfolios to improve outcomes.

Strategy 1: Focusing on short-dated high yield bonds

One way of seeking to minimise default risk on high yield bonds is to target assets which only have a short term until maturity.

When assigning a credit rating, rating agencies assign a rating for the whole issuer curve regardless of maturity. This often means that the credit rating overstates the probability of default for short-dated bonds.

Furthermore, it is much easier to forecast an issuer’s expected cashflows and liquidity requirements over the short term, so the analyst can be more confident that an issuer will be able to fund the maturity repayment for the bond or redeem the debt as expected at the first call date.

In some cases, subordinated bonds may mature before higher-rated longer-term debt, meaning that they benefit from temporal seniority.

Providing the outlook for the issuer looks acceptable, the portfolio can expect to hold bonds to maturity (or earlier call date) and thus does not need to incur a high degree of turnover, helping to mitigate the lower liquidity in this market.

A robust credit approach, focusing on identifying bonds that meet the above requirements, can help to mitigate losses from defaults. For example, such an approach might reflect that:

- telecoms companies tend to have consistent cashflows as consumers are reluctant to give up their mobile phones even during a recession;

- packaging companies can benefit during recessions as they benefit from non-discretionary demand; and

- some companies build cash piles well in advance of debt maturities, reducing risk of default for shorter-dated bonds.

Strategy 2: Focusing on fallen angels

‘Fallen angels’ are a subset of the high yield bond universe, consisting of bonds which were recently downgraded from investment grade to high yield status.

Fallen angels are often large multi-nationals with large capital structures, whereas traditional high yield-rated companies tend to be smaller businesses with less access to capital markets. For example, the larger fallen angels currently in the index include some household names from the automotive manufacture, airline and telecoms sectors.

Upon downgrade, many of these corporations are incentivised to repair their fundamentals to regain access to cheaper capital. As such, intuitively and empirically, we believe fallen angels are potentially stronger candidates to be upgraded to become investment grade issuers again – known as ‘rising stars’.

Fallen angels have historically outperformed other high yield bonds in an economic recovery, and fallen by less in a negative market for credit[1]. This phenomenon may be linked to a market overreaction and disproportionate spread-widening when a bond is downgraded, driven by forced selling from passive investment grade-focused accounts.

Historically, rising stars are almost twice as likely to have been fallen angels than constituents of the broader high yield market.[2]

Fallen angels may therefore provide insurers with exposure to the high yield sector but with higher credit ratings (predominantly BB), bear lower risks than the broader high yield market, and offer greater upside potential.

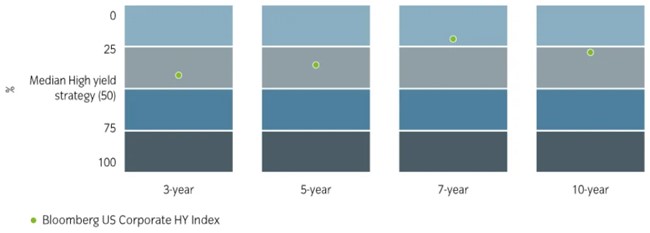

Strategy 3: Managing liquidity in the high yield market

One of the barriers to high yield investment for some insurers is the lower liquidity in the asset class, with bid-offer spreads typically 60bp to 80bp. This has resulted in many active and passive strategies underperforming the index over the medium and long term (see chart below for a US high yield comparison).