After a long post global financial crisis lull of low inflation, low interest rates and tepid fixed income performance are credit investors entering a new golden age?

For Insight portfolio manager Shaun Casey, the return of sustained inflationary pressures and higher interest rates has brought a fillip to credit markets, with surging demand for assets such as IG credit creating a range of potentially attractive new investment opportunities.

“We can see a path for credit continuing to perform very well, particularly in areas such as IG, in the coming months and quarters. We are seeing numerous investors coming into the asset class who haven’t been involved in fixed income for the last decade,” he says.

That increased demand coupled with a surprisingly resilient global economy, adds Casey, has largely seen off the effects of recent central bank interest rate intervention.

“In the current climate, we believe credit is quite an attractive investment. That said, investors should always think very carefully about their specific allocations when building out credit portfolios.”

Casey says much of the attractiveness of credit markets depends on the type of investor allocating to fixed income. Flexible investors with more nimble allocation strategies, he adds, could find themselves well placed to benefit from their exposure to credit.

“If you look at some of the yields on credit for more flexible investors allocating to fixed income, we believe we are seeing some of the best opportunities in over a decade, with yields having spiked considerably higher in the last two years. For bond investors, the additional compensation you receive for owning credit over government bonds can be a key factor in any underlying investment decision.”

From a sectoral perspective, Casey believes the banking sector offers some strong potential credit opportunity. Despite some high-profile problems in banking last year, particularly among some smaller US regional banks, Casey believes the sector is well regulated and could offer significant value to select investors.

“We don’t feel last year’s banking sector problems were systemic so much as down to short term management problems. In our view financial regulators have, on the whole, done a good job since the financial crisis in terms of making banking much safer and less risk prone. Last year saw further incremental change that has also tightened regulations still further.

“In our view, gaining more exposure to banks relative to non-financial corporates looks an attractive proposition as those recent sectoral defaults move further into the past and markets begin to price out some of the excess premium they are demanding for banks. We believe banks look in good shape and valuations remain relatively cheap,” he adds.

High yield outlook

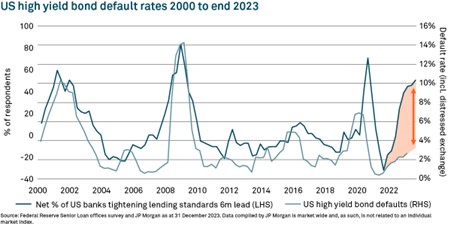

Across the credit universe, Casey also sees significant potential in some areas of the high yield debt market. However, he remains cautious on a market which has seen surprisingly low default levels in recent months.

“One of the big questions in the high yield market is: where have the defaults gone? It might be tempting for some to think ‘this time is different’. Yet from our standpoint those are four of the scariest words we feel can be used in investing. We would really need to see a long period of reliable and favourable default data to feel very confident we are not going to see an uptick in high yield defaults going forward.

“That said, and despite the fact high yield spreads are trading at multi-year ‘tights’ when compared to their IG credit peers, we do believe there is some significant opportunity in the high yield sector. If you have the analytical strength to drill into individual balance sheets and identify those corporate names that are going to survive and thrive, it can be possible to find some very attractive and interesting investments.”